Investing in your pension is one of the most important financial decisions you'll make in your lifetime.

Here’s five quick tips to make sure you’re making the most of yours.

For readers in a rush:

- The sooner you contribute the better. Thanks to the benefits of compounding.

- The government will give you free money when you contribute to a pension.

- Your workplace will also give you free money. And they might put more money into your pension if you also contribute more.

- You should decide on whether you’re comfortable managing your pension investments yourself, or whether you want your provider to.

- Make sure you’re aware of pension scams and how to make sure you stay protected and aware.

Tip 1: Start Early and Contribute Regularly

The sooner you start contributing to your pension, the better.

That’s because even small, regular contributions can grow over time. All thanks to something called compounding.

Compounding, in simple terms, is all about earning money on your money. When you put money into your pension, you earn a return on it (growth). You also earn a return on both that initial amount, and the growth it makes.

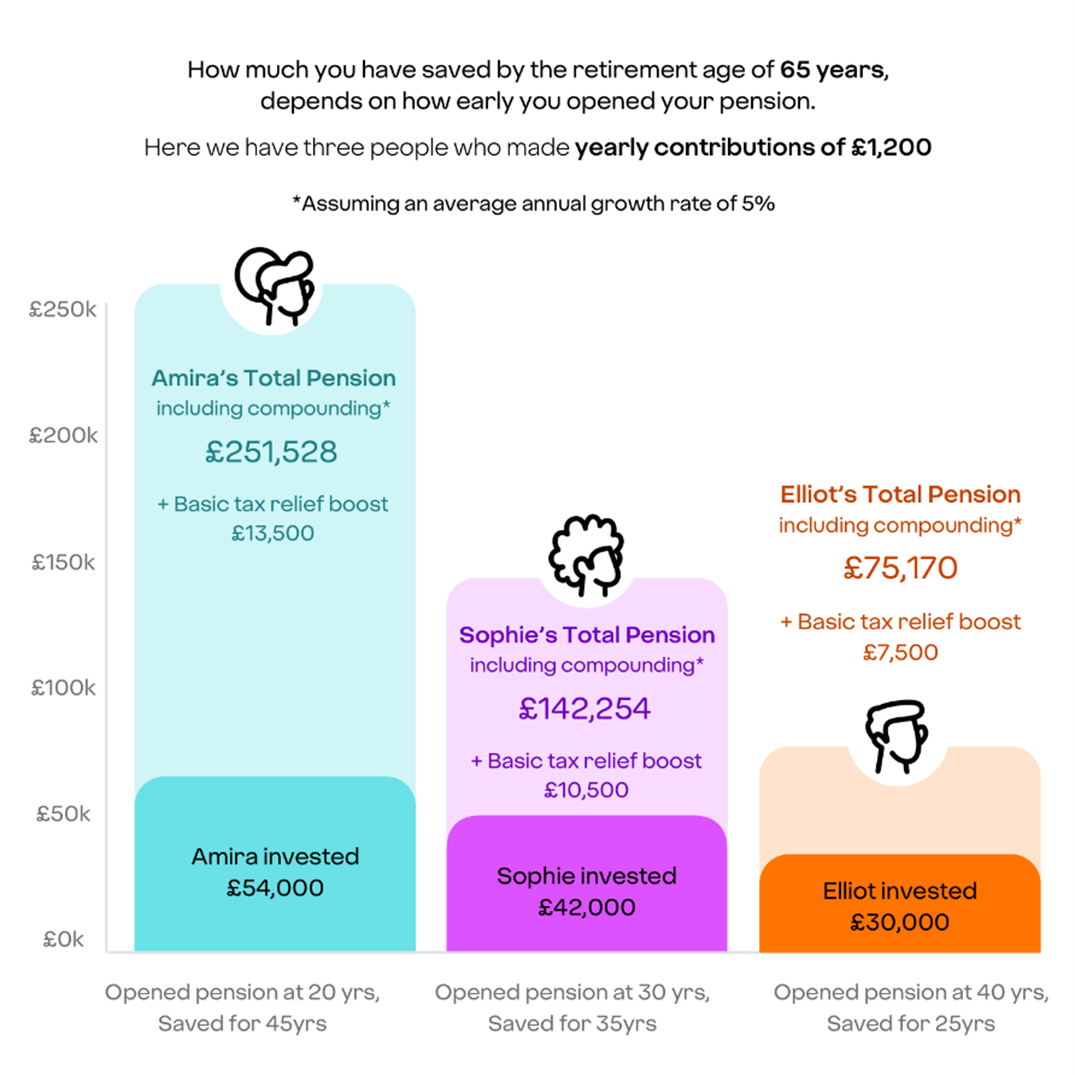

The graph below gives you an idea of what could happens if three people saved into their pension at different times. How long and how much you save will impact how much your pension will grow.

Tip 2: Remember you get a tax boost

When you add money into a pension, you benefit from tax relief. This means the government boosts your pension pot by some of the tax you would have paid to them on your contribution.

For basic-rate taxpayers, this means for every £100 you pay in, it would only cost you £80. If you’re a higher rate taxpayer, that £100 would only cost you £60. And if you’re an additional rate taxpayer that £100 would only cost you £55.

The basic rate of tax relief is usually claimed on your behalf by your provider. If you’re a higher or additional rate taxpayer, you claim any extra relief through your tax return or by contacting HMRC.

You can usually backdate any higher or additional rate tax relief for the previous four tax years.

Who doesn’t love free money?

3. Maximise your workplace pensions

If you’re employed in the UK, there’s a good chance your workplace has a pension scheme for employees.

Here’s the fun part:

- You’ll be automatically enrolled onto a workplace pension if you work in the UK. If you’re aged between 22 and State pension age. And you earn at least £10,000 per year.

- Under the Auto-Enrolment scheme, employers must pay at least 3% of your qualifying earnings into your pension.

- You automatically contribute 5% into your workplace pension. Unless you opt-out.

- Some employers will offer you the option to contribute more to your pension. They may also offer to increase their contributions when you do. The more you pay into your pension, the more they do too.

4. Think about being hands off… or hands on

Regularly reviewing your pension plan should be part of your normal regular financial health check.

Life changes, such as marriage, children, or changes in income, can affect how much you can or should contribute to your pension.

But you can decide whether you want to be involved in the investment options and retirement planning for your pension. Or whether you’d prefer if someone did this for you.

This could look like having a pension that automatically analyses your investments based on your age and changes them based on your life stage.

There’s a little more work involved when it comes to choosing your own investments. Make sure you’re comfortable before deciding to take hold of the reins.

5. Be aware of pension scams

It might feel like a pension scam could never happen to you. But there’s a few things you should do to reduce your risk of getting scammed:

1. Be wary of unsolicited offers and schemes that promise high returns with little risk. These are usually under the guise of making a lot of financial gains.

2. Don’t give out any of your personal information until you verify whether the financial advisors and firms you deal with are legitimate.

You can find The Financial Conduct Authority (FCA) provides register of approved firms here.