What's changed?

The Financial Conduct Authority (FCA) have undertaken a study looking at how customers use their credit cards. As a result, credit card providers are working on putting additional support in place to help customers clear debt quickly and avoid incurring additional interest and fees.

The support being introduced includes letting you know when you are reaching your credit limit, providing you with the option to change your payment date, giving you greater control over increases in your credit limit, and raising awareness of persistent debt.

What is Persistent Debt?

The FCA have introduced the definition of persistent debt, and measures to help customers affected by persistent debt, to address the problem of carrying a balance over a long period of time, which can be costly, if the balance is not being repaid in a timely manner.

The definition of persistent debt, as set out by the Financial Conduct Authority (FCA), is where, over a period of 18 months, a customer pays more in interest, fees and charges than repaid from their credit card balance.

Typically, this is because the customer is making just the minimum payment each month on their credit card. As a result the majority of the payment covers the interest, fees and charges with only a small amount towards repaying the balance.

What does Persistent Debt mean for me?

If we believe your account is in ‘persistent debt’ we will write to you to ask if you can afford to increase your monthly repayments. The more you pay each month, the quicker you will clear your balance and the less you will pay in interest.

You can see how much interest you could potentially save, or how much quicker you could clear your balance by using this calculator, available at www.cardcosts.org.uk

When using the calculator:

- Input your current balance (the amount you owe on your card)

- Input the interest rate you are paying

- Input the amount you intend to spend each month on your card.

Your current balance and the interest rates you are paying can be found on your last statement. If you have different interest rates then just take an average rate for the purposes of the calculation.

The calculator can then be adjusted to select the different ways you want to repay e.g. repay a fixed amount each month.

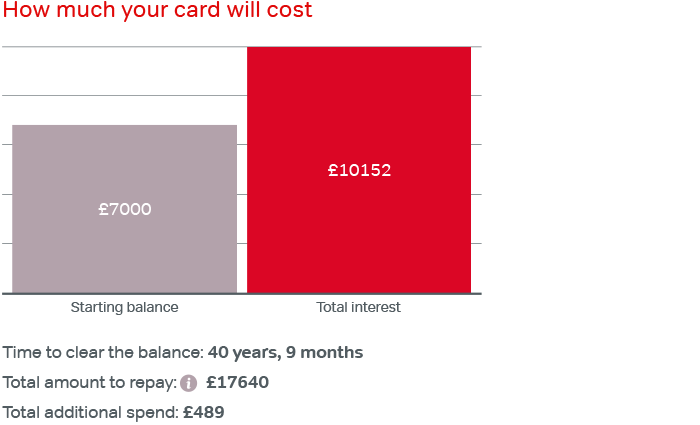

If you select the option ‘pay the minimum amount’, this should show you roughly what you are paying now, and how long it will take you to repay your balance, as well as the interest you are likely to pay. The example below shows you how long it would take to pay off £7,000 if you are only paying the minimum amount.

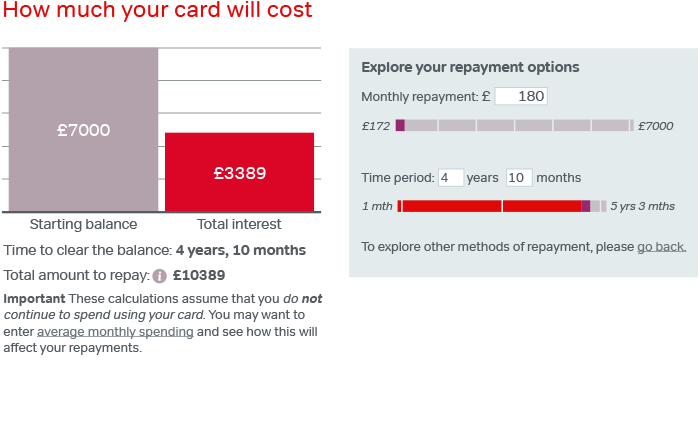

To avoid being in persistent debt, your monthly payment needs to be high enough to pay more off your outstanding balance than you are paying in fees and interest. Ideally, you need to increase the monthly payment amount in the calculator until the Starting Balance amount (which is the amount you owe on your card) is higher than the Total Interest amount, as shown in the example below. If you do this, and then make that monthly payment on your Virgin Money Credit Card, you won’t be in persistent debt so long as you stick to the increased monthly payment and don’t spend more on your card each month.

Use the calculator and try some different scenarios to find the payment amount that feels right for you and that you can afford. Once you know how much extra you’d like to pay each month, you can give us a call to increase your monthly Direct Debit. Alternatively, if you pay each month by another route, just continue to pay that way but make sure you pay the increased amount with effect from next month’s payment.

(If you want to make changes, we do have more information available about managing your Direct Debit).

If you are able to increase your monthly payment by enough to mean your account is no longer classed as being in ‘persistent debt’, we won’t need to contact you again about possible further steps.

FootnoteExample graphs calculated using an outstanding balance of £7,000, with an interest rate of 18.9% and minimum payment rules are 2.5%, or £5 whichever is the highest.

What if I can’t afford to increase my monthly payment?

If, after writing to you, you continue to have paid more in interest, fees and charges than paid off your balance for a further 9 months then your account will still be classed as being in ‘persistent debt’. We will write to you again at this point to again discuss the benefits of increasing your monthly payment, and your options if you are unable to do so.

If you are still in persistent debt 18 months after we have first written to you your account will be classed as being in ‘extended persistent debt’. If you are unable to increase your monthly payment, or have chosen not to increase it, before this time we will be able to take further steps to help you out of persistent debt, such as:

- increasing your minimum payment;

- suspending or cancelling your card, which may affect your credit rating and influence your ability to get credit elsewhere.

As a responsible lender, we want to look after you and make sure you have the opportunity to tell us if you need any help. So if your account is in arrears or over its credit limit, you’re having trouble making your minimum payment or you can’t afford to increase the amount you pay each month, please get in touch on 0800 678 1636.

You can also get advice from a number of charities or not-for-profit organisations (like the ones listed below).

- National Debtline Tel: 0808 808 4000 www.nationaldebtline.org

- StepChange Debt Charity Tel: 0800 138 1111 www.stepchange.org

- Citizens Advice Bureau Tel: Call the Local Office www.citizensadvice.org.uk

- Payplan Tel: 0800 280 2816 www.payplan.co.uk

- MoneyHelper Tel: 0800 138 7777 www.moneyhelper.org.uk

Calls to 0800 numbers are free from personal mobile phones and residential UK landlines. Calls will be monitored and recorded.

Some things to consider

There are a few things to consider to help avoid going into persistent debt:

- consider increasing your repayments, if you can; this will help to reduce the length of time it takes you to pay down your outstanding balance;

- consider whether changing your repayment date may help; this will give you more control over your repayments and may help you to avoid late payment fees;

- consider changing your repayment method; this may make it easier for you to make repayments on time and for the amount you choose;

- and, remember please contact us if you ever want to discuss your options.