Q: If a pension is for when you retire, and you’ve got years and years before you get there, there’s not much point in saving for one when you’re younger, right?

A: Although a pension is designed for later life, typically after you stop working, the earlier you save into a pension, the better. There’s four reasons why:

1.You benefit from compound growth

2.You get free money

3.Your pension has longer to grow

4.You spend more time in the market to smooth out any ups and downs

Here’s why:

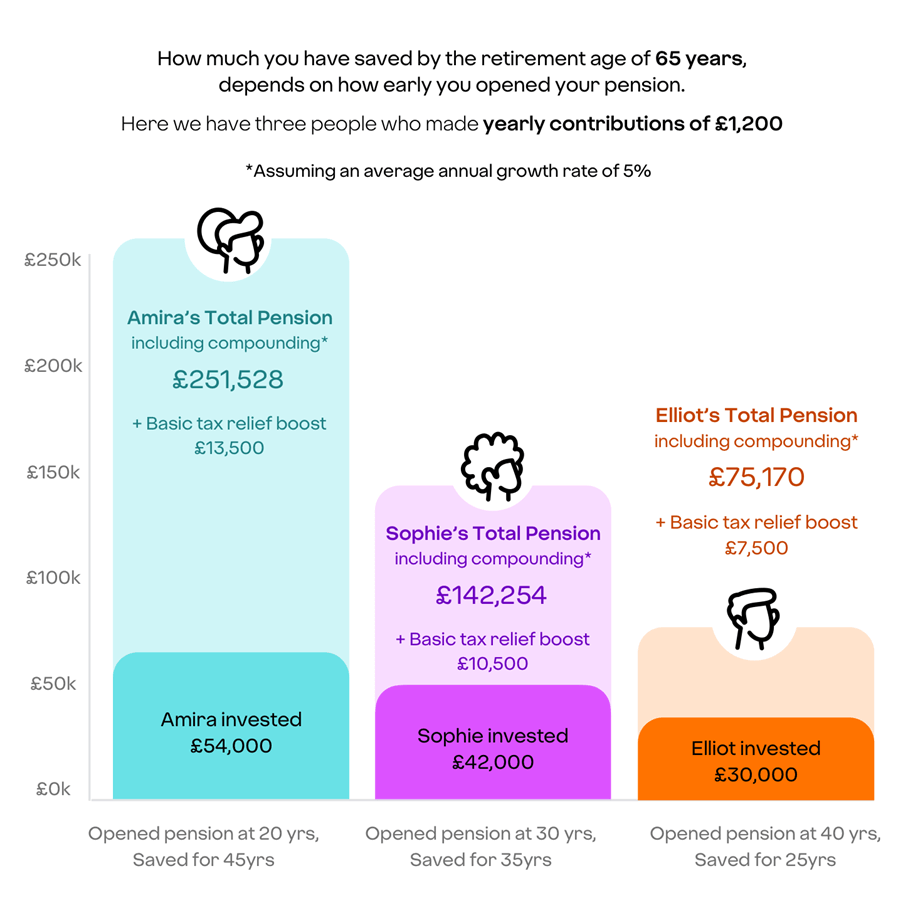

1. You take advantage of compound growth

The longer you save into a pension, the bigger the growth on your savings can be. That’s because, as well as evening out the ups and downs of the stock market, there’s more time for it to grow.

The growth you get from your pension benefits from compounding. A bit like the interest in a cash savings account.

It’s when you earn interest on both the initial money you’ve saved, as well as the interest your money has earned.

Let’s break it down

1.Amira pops £1,200 into a personal pension each year.

2.Suppose her investments grow evenly at a rate of 5% per year after all charges have been applied. . By the end of the year her £1,200 will have grown to £1,260.

3.In year two she pays in another £1,200 so she now has £2,460 invested. If that grows by another 5% (after charges), she’ll finish year two with £2,583.

That’s how compounding works.

2. You get free money

Yes really – it’s given to you through ‘tax relief’. If you’re a UK taxpayer, then the government will automatically top up payments you make to your pension. If you’re a basic rate (20%) taxpayer, it means that every £100 put into your pension only costs you £80. The government pay in the other £20.

So, let’s look at how that would affect Amira.

1.She puts £1,200 into her pension each year.

2.The government adds basic rate tax relief to her contributions, a topping it up by an extra £300 - giving her a total of £1,500 in contributions.

3.That 5% growth (after charges) in year one will now equal £75, so by the end of the year she’ll have £1,575.

4.And in year two Amira contributes another £1,200 to her pot, and the government adds another £300 to that. Her total pot now stands at £3,075 invested. And if that grows by 5% again, she’ll make £154 of growth – giving her a grand total of £3,229 by the end of year two.

*If you’re a higher or additional rate taxpayer then you could also receive another 20% or 25% in tax relief too. Find out more about pension tax relief here.